Decarbonization

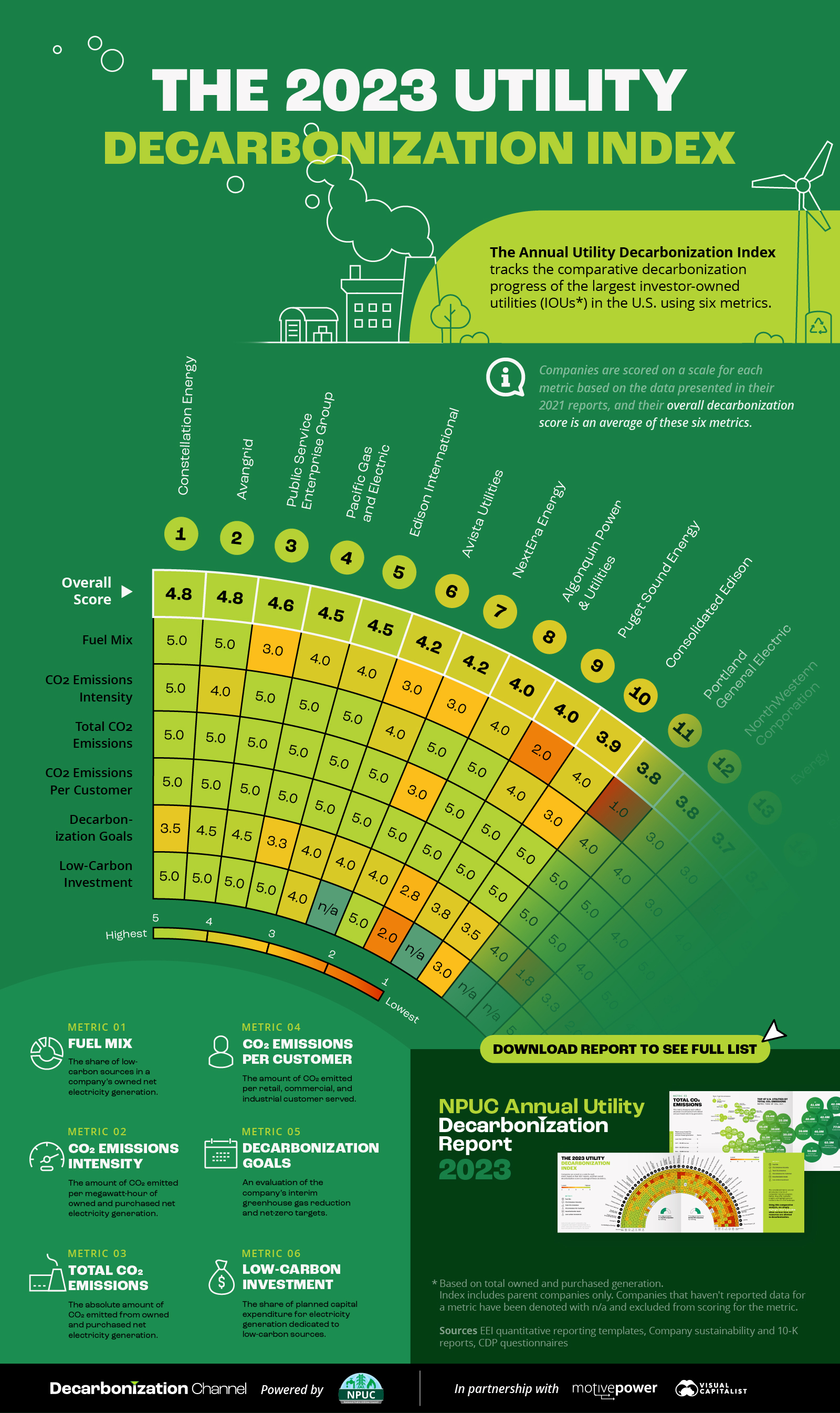

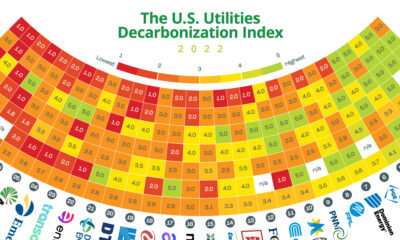

The 2023 Utility Decarbonization Index

The 2023 Utility Decarbonization Index

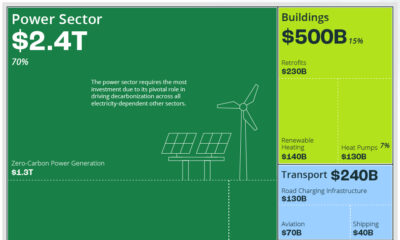

Electric utilities and the power sector have a pivotal role to play in decarbonizing the U.S. economy, especially with the electrification of sectors such as transportation.

So, where do the country’s largest electricity producers stand on the path to decarbonization?

In collaboration with our sponsor National Public Utilities Council, we present the 2023 edition of our Annual Utility Decarbonization Index. The index uses 2021 data (the latest available at the time of data collection) to track the comparative decarbonization progress of the 47 largest investor-owned utilities (IOUs) in the United States.

In the graphic above, we give a preview of the top 10 rankers.

Methodology of the Utility Decarbonization Index

The Utility Decarbonization Index uses the following six metrics to track decarbonization progress:

- Fuel Mix

The share of low-carbon sources in a utility’s owned net electricity generation. - CO2 Emissions Intensity

The amount of CO2 emitted per megawatt-hour of owned and purchased net electricity generation. - Total CO2 Emissions

The absolute amount of CO2 emitted from owned and purchased net electricity generation. - CO2 Emissions Per Customer

The amount of CO2 emitted per retail, commercial, and industrial customer served. - Decarbonization Goals

An evaluation of the company’s interim greenhouse gas reduction and net-zero targets, with a 50% reduction in emissions by 2030 and net-zero by 2050 as baseline targets. - Low-Carbon investment

The share of planned capital expenditure for electricity generation dedicated to low-carbon sources.

All 47 IOUs in the Decarbonization Index are scored on a scale of one (lowest) to five (highest) for each of the six metrics, indicating whether they are trailing or leading compared to their peers. A utility’s final decarbonization score is an average of its scores across the six metrics.

The data for these metrics comes from company sustainability reports, quantitative ESG reporting templates from the Edison Electric Institute, and the Climate Disclosure Project’s Climate Change Questionnaire filings.

With the methodology in mind, let’s take a look at the 10 utilities that are leading the ranking in this year’s Utility Decarbonization Index.

The Annual Utility Decarbonization Index 2023

The 47 IOUs ranked in the Index are the largest electricity producers in the country, together representing over 58% of U.S. electricity generation in 2021 and serving 68% of all US. electric customers. Therefore, the decarbonization of these utilities can have a massive impact on the power sector and other electricity-consuming sectors.

However, it’s important to note that a score of five on the Utility Decarbonization Index does not indicate full decarbonization or net-zero emissions. Rather, it indicates that the utility is leading in decarbonization relative to its peers.

Here are the top 10 IOUs in this year’s ranking:

| Rank | Company | Decarbonization score |

|---|---|---|

| #1 | Constellation Energy (Exelon) | 4.8 |

| #2 | Avangrid | 4.8 |

| #3 | Public Service Enterprise Group | 4.6 |

| #4 | Pacific Gas and Electric | 4.5 |

| #5 | Edison International (EIX) | 4.5 |

| #6 | Avista Utilities | 4.2 |

| #7 | NextEra Energy | 4.2 |

| #8 | Algonquin Power & Utilities | 4.0 |

| #9 | Puget Sound Energy (PSE) | 4.0 |

| #10 | Consolidated Edison | 3.9 |

Constellation Energy, a newly formed subsidiary of Exelon, tops this year’s Decarbonization Index along with Avangrid. Constellation is the largest low-carbon electricity producer among the 47 IOUs, with 80% of its owned net electricity generation coming from nuclear power plants. The company also had the lowest CO2 emissions intensity of all utilities in the Index.

Avangrid, a clean energy-focused utility operating in the Northeast, ties for first place thanks to its low-carbon fuel mix and ambitious decarbonization targets to achieve carbon neutrality in Scope 1 and 2 emissions by 2030.

Download the 2023 Annual Utility Decarbonization Report

Are you interested in seeing the rest of the rankings? Check out the full report!

In addition to the Decarbonization Index, there’s much more to unpack, including:

- Six reasons why utilities must decarbonize

- Highlights and challenges to decarbonization from 2021–2022

- The data behind the six individual metrics

- The U.S. Utilities ESG report card

- Decarbonization strategies for U.S. utilities

Download the 2023 NPUC Annual Utility Decarbonization Report and find out everything you need to know about utility decarbonization.

Decarbonization

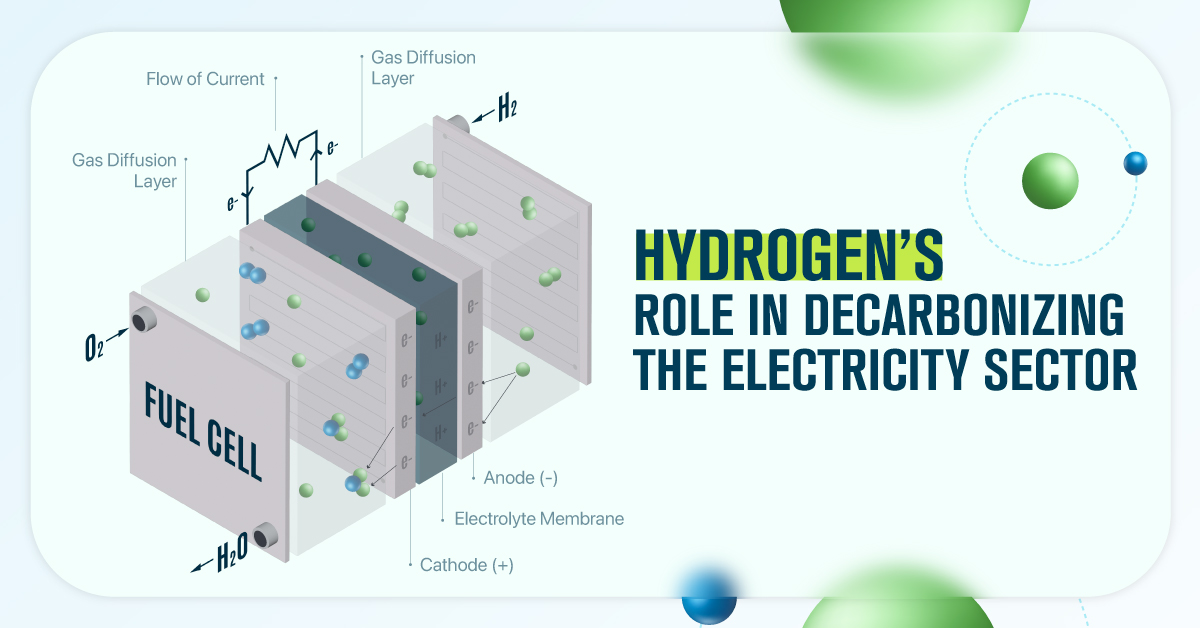

Unpacking Hydrogen’s Role in Decarbonizing the Electricity Sector

In this infographic, we discuss three ways hydrogen can support the decarbonization of the global electricity sector.

Hydrogen’s Role in Decarbonizing the Electricity Sector

Hydrogen constitutes 75% of the elemental mass in our universe.

According to the International Energy Agency (IEA), it could also play a pivotal role in global decarbonization efforts.

This infographic, created in partnership with the National Public Utilities Council, explores three ways this element could support the decarbonization of the global electricity sector.

Hydrogen 101

First, let’s get a few basics about hydrogen out of the way.

While abundant in nature, hydrogen is rarely found in its elemental state (H2) on Earth, meaning that it needs to be separated from other chemical compounds, such as water (H2O). Once extracted, however, it becomes a versatile and energy-dense fuel source, containing approximately three times the energy content of gasoline or natural gas.

There are several methods to extract hydrogen from compounds. Depending on the production method and energy source, the resulting hydrogen is often categorized by color to show its emission impact.

| Color | Hydrogen Production Method | Energy Source |

|---|---|---|

| Black | Gasification | Coal or Lignite |

| Gray | Steam Methane Reforming (SMR) | Natural Gas |

| Blue | SMR + Carbon Capture and Storage (CCS) | Natural Gas |

| Purple* | Electrolysis | Nuclear Energy |

| Green | Electrolysis | Renewable Energy |

*Purple hydrogen is also referred to as red or pink hydrogen.

Today, black, gray, and blue hydrogen are used in emission-heavy industries such as petroleum refining and ammonia production.

The technology and infrastructure for purple and green hydrogen, on the other hand, are still taking shape. As they progress, these emission-free sources of hydrogen are expected to play a pivotal role in decarbonizing many hard-to-abate sectors, including power.

Three Ways Green Hydrogen Can Help Decarbonize

Now that we’ve covered hydrogen basics, let’s dive into where emission-free hydrogen can fit in the race to decarbonize our global electricity system.

#1: Hydrogen and Natural Gas Blending

Hydrogen can be blended with natural gas in existing pipeline infrastructure for lower-emission power generation.

According to Jenbacher, a 20–30% hydrogen volume can lead to a 7–11% decrease in CO2 emissions, compared to natural gas on its own.

In 2022, U.S. electricity from natural gas generated 743 million metric tons in the United States. A 9% reduction in emissions through hydrogen blending lowers emissions by 67 million metric tons CO2, all without the need to build new infrastructure.

#2: Fuel Cells

A fuel cell generates electricity through an electrochemical reaction between hydrogen and oxygen, with water as the only byproduct.

By using green or pink hydrogen, fuel cells can provide 100% emission-free electricity that is also efficient, reliable, and dispatchable.

#3: Energy Storage

Energy storage plays a pivotal role in decarbonizing the power sector by balancing the intermittent nature of renewables.

While other technologies, such as lithium-ion batteries, can also provide energy storage, hydrogen has a greater potential to offer both large-scale and long-term storage, up to several months at a time.

As technology advances, the IEA predicts that global underground hydrogen capacity will grow by more than 200,000% in the next 30 years, reaching 1,200 TWh in 2050. That amount of energy can power 70,000 U.S. homes for an entire year, underscoring the untapped potential that lies within hydrogen.

Learn how the National Public Utilities Council is working towards the future of sustainable electricity.

Climate

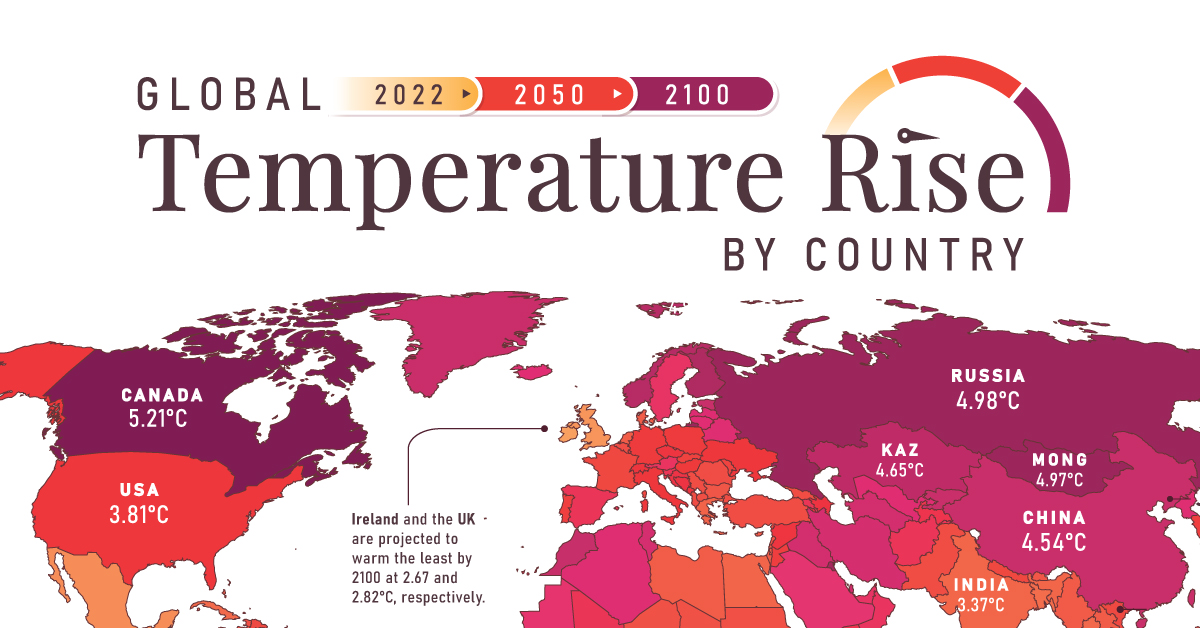

Mapped: Global Temperature Rise by Country (2022-2100P)

In this set of three maps, we show the global temperature rise on a national level for 2022, 2050, and 2100 based on an analysis by Berkeley Earth.

Mapped: Global Temperature Rise by Country (2022-2100P)

Many scientific authorities, such as the Intergovernmental Panel on Climate Change (IPCC), often discuss the need to limit planetary warming to 2°C above pre-industrial levels.

But did you know that this warming will not be evenly distributed throughout the globe due to factors such as geography, weather patterns, ocean currents, and the influence of human activities?

To discover the current and projected nuances of this uneven warming, these three maps created in partnership with the National Public Utilities Council visualize the global temperature rise by country, using new and updated data from Berkeley Earth.

Current State of Warming

The three maps above visualize warming relative to each country’s average 1850-1900 temperatures.

Looking at warming in 2022, we see that average national warming (i.e. warming excluding oceans) is already 1.81°C above those numbers, with Mongolia warming the most (2.54°C) and Bangladesh warming the least (1.1°C).

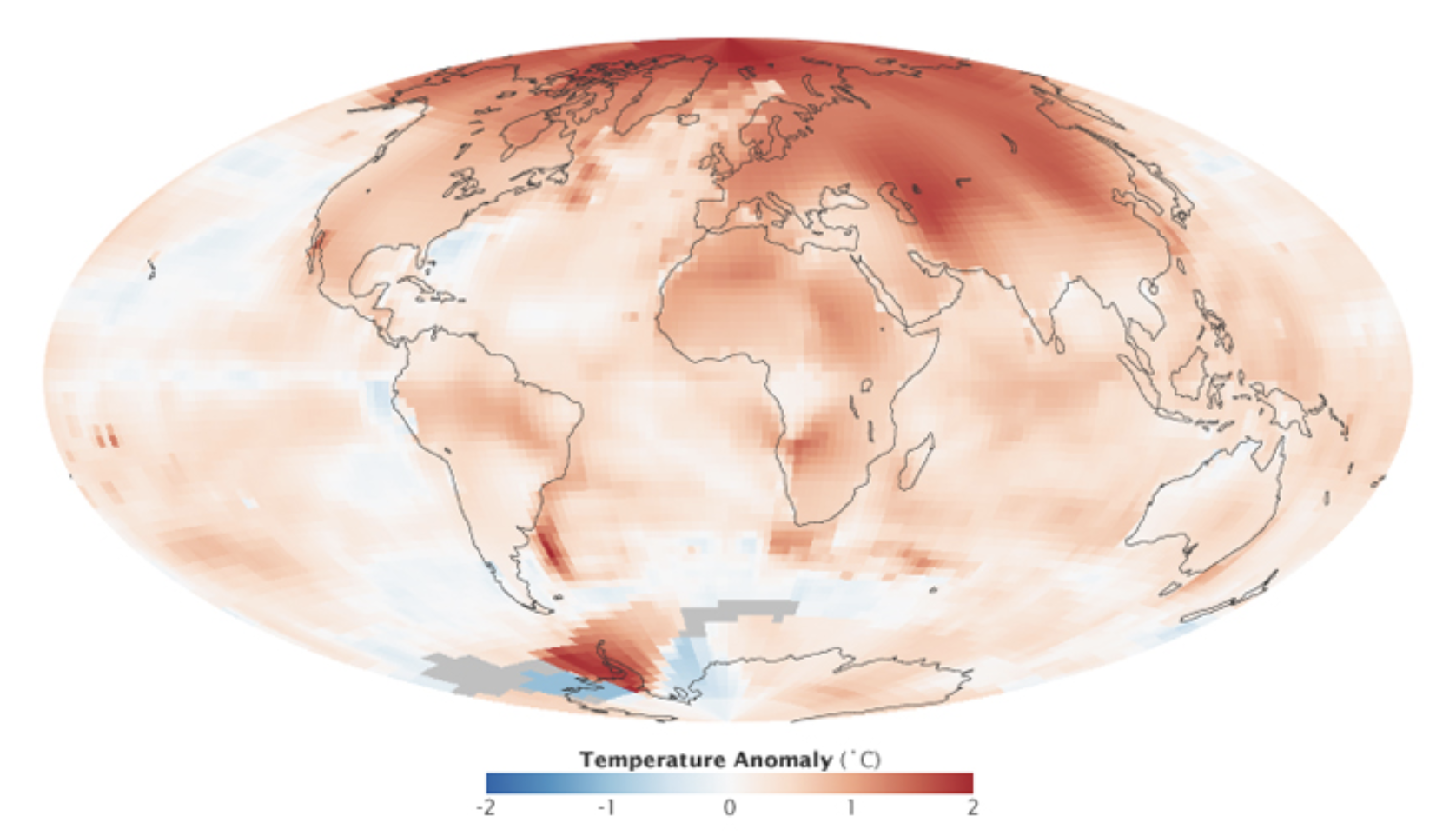

As the map depicts, warming is generally more accelerated in the Global North. One of the reasons for this is Arctic amplification.

Arctic amplification refers to the disproportionate heating experienced in the Arctic compared to the rest of the planet. This amplification is fueled by multiple feedback loops, including decreased albedo as ice cover diminishes, leading to further absorption of heat and exacerbating the warming effect.

Arctic amplification. Source: NASA

Aside from modern-day observations, the effects of Arctic amplification are also clearly seen in climate models, where accelerated warming in countries such as Russia and Canada is seen through 2100.

Projected Warming in 2050 and 2100

Moving over to the second and third maps in the slides above, we discover country-level 2050 and 2100 warming projections.

These projections are based on the IPCC’s “middle-of-the-road” scenario, titled Shared Socioeconomic Pathway (SSP) 2-4.5. Out of the various established pathways, this one is the closest to expected emissions under current policies.

2050 Projections

Under the SSP2-4.5 scenario, average national warming is projected to be 2.75°C above average 1850-1900 temperatures in 2050. This includes Mongolia, with the most substantial warming of 3.76°C, and New Zealand, with the mildest warming of 2.02°C.

To put those temperatures into context, here are the risks that would likely accompany them, according to the IPCC’s latest assessment report.

- Extreme weather events will be more frequent and intense, including heavy precipitation and related flooding and cyclones.

- Nearly all ecosystems will face high risks of biodiversity loss, including terrestrial, freshwater, coastal and marine ecosystems.

- Accelerated sea level rise will threaten coastal cities, leading to mass displacement.

Let’s now take a look at 2100 projections, which would have significantly higher levels of risk unless fast and extreme mitigation and adaptation measures are implemented in the upcoming decades.

2100 Projections

2100 projections under the SSP2-4.5 scenario depict an average national warming of 3.80°C.

More than 55 countries across the globe are projected to have warming above 4°C in comparison to their 1850-1900 averages, and nearly 100 above 3.5°C.

Here is what those levels of warming would likely mean, according to the IPCC.

- 3-39% of terrestrial species will face very high risks of extinction.

- Water scarcity will considerably affect cities, farms, and hydro plants, and about 10% of the world’s land area will experience rises in both exceptionally high and exceptionally low river flows.

- Droughts, floods, and heatwaves will pose substantial threats to global food production and accessibility, eroding food security and impacting nutritional stability on a significant scale.

Generally, warming at this level is expected to pose substantial catastrophic risks to humanity, necessitating swift and bold climate action.

Learn more about how electric utilities and the power sector can lead on the path toward decarbonization here.

-

Electrification1 year ago

Electrification1 year agoVisualized: How the Power Grid Works

-

Energy Shift9 months ago

Energy Shift9 months agoRanked: The Cheapest Sources of Electricity in the U.S.

-

Energy Shift1 year ago

Energy Shift1 year agoAnimated: 70 Years of U.S. Electricity Generation by Source

-

Clean Energy1 year ago

Clean Energy1 year agoBreaking Down Clean Energy Funding in the Inflation Reduction Act

-

Emissions1 year ago

Emissions1 year agoVisualizing Global Per Capita CO2 Emissions

-

Decarbonization1 year ago

Decarbonization1 year agoThe U.S. Utilities Decarbonization Index

-

Clean Energy1 year ago

Clean Energy1 year agoThe 30 Largest U.S. Hydropower Plants

-

Clean Energy7 months ago

Clean Energy7 months agoBreaking Down the $110 Trillion Cost of the Clean Energy Transition